Artemis Gold Announces Results of Expansion Study for Blackwater Mine

February 21, 2024

Study outlines opportunity to accelerate expansion; advancing a Tier 1 asset

All amounts in Canadian dollars except where otherwise noted

- After-tax NPV of C$3.25 billion at long-term gold price of US$1,800 per ounce (“oz”), after taking into account repayment of Phase 1 Project Loan Facility (“PLF”), as well as the effect of the gold and silver streams

- Greater than 500,000 gold equivalent (“AuEq”) oz average annual production for first 10 years

- Average all-in sustaining costs (“AISC”) of US$712/oz gold for first 10 years, placing Blackwater in lowest decile of the global cost curve for gold mines

- Average annual free cash flow of approximately C$500 million for first 10 years

- Potential for mine life extension

Vancouver, British Columbia – Artemis Gold Inc. (TSX-V: ARTG) (“Artemis Gold” or the “Company”) announces the results of an expansion study for the Blackwater Mine in Central British Columbia. Blackwater is a world-class, large-scale advanced development project in a tier-one mining jurisdiction.

The construction of the Phase 1 processing plant of 6 million tonnes per annum (“Mtpa”) is well advanced, and the expansion study considers that Phase 1 has been completed. The purpose of the expansion study is to optimize the timing of mine expansion through the advancing of Phase 2 to year 3 of operations at an increased production capacity of 15 Mtpa, and Phase 3 to year 7 of operations at an increased production capacity of 25 Mtpa. The expansions are expected to be funded from operating cash flows based on the input assumptions of the expansion study.

The expansion study is based on Blackwater’s existing Proven and Probable Mineral Reserves and no changes were made to the Mineral Reserve and Mineral Resource estimates. The relevant capital and operating estimates have been updated to reflect 2024 cost estimates. The Company’s Board of Directors is yet to commit to the acceleration of the Phase 2 expansion. A decision is expected to be considered in H2 2024.

Table 1 – Key Results of Expansion Study

| Metric | Units | First 5 years | First 10 years | LOM |

| Average annual production | AuEq oz1 | 488,000 | 506,000 | 469,000 |

| Average AISC2 per gold ounce | US$/oz | US$615 | US$712 | US$781 |

| Average annual free cash flow3 | C$ | C$552M | C$489M | C$413M |

Notes

- The Company expects to produce gold and silver doré. Gold equivalent ounces have been determined using a gold:silver ratio of 78:1 (or US$1,800:US$23)

- AISC includes selling costs, royalty payments, operating costs, sustaining capital and closure costs, less silver by-product credits and adjustments to stockpile inventory, divided by payable gold ounces

- Free cash flow = operating cash flow less sustaining capex, closure costs and taxes

Table 2 – Operating and Financial Results of Expansion Study

| Units | First 5 years | First 10 years | LOM (17 years) | |

| Average throughput capacity | Mtpa | 12 | 18 | 20 |

| Gold grade | g/t | 1.29 | 0.91 | 0.75 |

| Silver grade | g/t | 7.75 | 5.92 | 5.78 |

| Gold equivalent grade | AuEq g/t1 | 1.36 | 0.96 | 0.79 |

| Gold recoveries | % | 93% | 93% | 93% |

| Average annual gold production | Au oz | 463,000 | 478,000 | 438,000 |

| Average annual silver production | Ag oz | 1,944,000 | 2,165,000 | 2,376,000 |

| Average annual AuEq production | AuEq oz2 | 488,000 | 506,000 | 469,000 |

| Strip ratio | Waste:Ore | 1.99 | 2.13 | 2.01 |

| Growth capital3,4 | C$ | C$1,174M | C$1,497M | C$1,497M |

| Sustaining capital4 | C$ | C$499M | C$874M | C$1,122M |

| Operating costs | C$/tonne milled | C$26.86 | C$23.00 | C$20.03 |

| Cash costs5 | US$/oz | US$456 | US$577 | US$645 |

| AISC6 | US$/oz | US$615 | US$712 | US$781 |

| Average annual free cash flow7 | C$ | C$552M | C$489M | C$413M |

| After-tax NPV5%8 | C$ | C$3.25B | ||

Notes

- Gold equivalent grades have been determined using a gold price of US$1,800/oz, a silver price of US$23/oz, a gold metallurgical recovery of 93%, a silver metallurgical recovery of 65%, and mining smelter terms for the following equation: AuEq = Au g/t + (Ag g/t x 0.0085)

- Gold equivalent ounces have been determined using a gold-to-silver ratio of 78:1 (US$1,800:US$23)

- Includes deferred initial capex

- Excludes closure costs and salvage value

- Cash costs include selling costs, royalty payments, operating costs, less silver by-product credits and adjustments to stockpile inventory, divided by payable gold ounces

- AISC includes cash costs as defined above, sustaining capital and closure costs, divided by payable gold ounces

- Free cash flow = operating cash flow less sustaining capex, closure costs and taxes

- After-tax NPV represents the net present value of after-tax project cash flows, discounted at a rate of 5%. The after-tax project cash flows take into account the repayment of the PLF of $385 million, as well as the effect of the gold stream and silver stream arrangements

Phase 1 Investments

In Q2 2023, Artemis Gold announced additional investments of approximately C$50 million in the Phase 1 scope of work to facilitate the potential fast-tracking of Phase 2. These additional investments were included in the Phase 1 guided initial capital cost of C$730-C$750 million and included additional structural steel and increased conveyor belt widths in the crushing circuits, as well as the introduction of variable-speed drives to the ball mill. Selected electrical components were also upgraded to facilitate the Phase 2 requirements and to include optionality in relation to the use of redundancy backup power sources. Other Phase 1 optimizations included upsizing of the oxygen plant coupled with down-shaft-sparging of oxygen to the pre-leach and carbon-in-leach (“CIL”) trains, along with the optimization of the CIL layout to facilitate non-intrusive expansion to Phase 2, as well as full conversion of the detoxification process to remove the need for tanker-supplied liquid sulphur dioxide. At the end of December 2023, C$389 million of the guided initial capital had been spent, and C$615 million, or 84% of the lower end of the guided capital range, was fully contractually committed.

For the expansion study, the Phase 1 guided initial capital costs are considered to have been spent and are not included in the reported net present value. The net present value is reported net of the scheduled repayment of the PLF associated with Phase 1 of C$385 million and all gold and silver stream participations.

Infrastructure

On completion of Phase 1, the majority of infrastructure requirements for the Phase 2 expansion will already be in place, including the primary crushing circuit, water storage and distribution, hydro-electric power, maintenance workshops, laboratory, site administration buildings, warehouse and workforce facilities. Additional infrastructure required for Phase 2 includes a secondary crushing circuit, crushed ore stockpile, a second ball mill, a semi-autogenous (“SAG”) grinding mill, the associated expansion of the mill, gold recovery and reagent buildings, additional leach and CIL tanks, expansion of the elution circuit, as well as the associated expansion of mobile maintenance infrastructure to support additional mining equipment.

Mining

The expansion study mine plan considers conventional open pit mining methods (drill-blast-load-haul) in all phases. Open pit mining operations are anticipated to run for 15 years, excluding pre-production mining. Following mining operations, stockpiled low-grade material is expected to be processed for an additional two years, resulting in a total mine life of 17 years. The open pit would be developed with a series of pushbacks. The initial stages would expose near-surface, high-grade, lower-strip-ratio ore providing mill feed over the early years of the project. The remaining stages expand the pit to the north and south, targeting progressively deeper ore.

Owner-managed mining and fleet maintenance operations are planned for 365 days/year, with two 12-hour shifts planned per day. Contractor drill and blast services are planned for the first three years of operations, with drill operations converting to an owner-operated function thereafter, and contractor blasting services continuing throughout the remaining life of operations. Mining will be undertaken using 600-tonne class hydraulic shovels, 400-tonne class hydraulic excavators, and 240-tonne payload class haul trucks. The initial drill and loading fleets are planned to be diesel-drive, with the expansion fleet for drill and loading being electric-drive. The haul fleet is currently assumed to be diesel-drive for the entire life of mine (“LOM”). The initial mine equipment fleet is paid back through a lease arrangement with the supplier the expansion fleet being funded from operating cash flows.

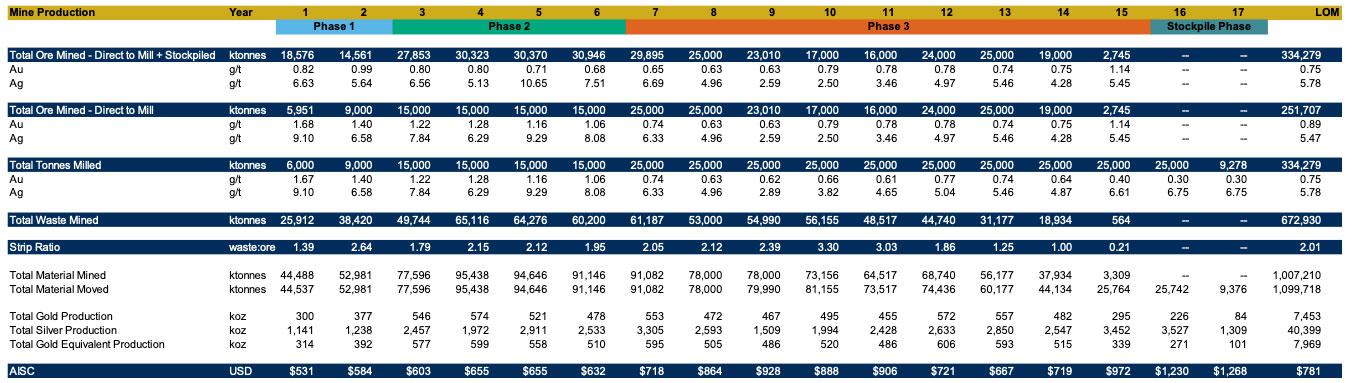

Details of mining volumes and material movements contemplated in the expansion study are included in Appendix A to this news release.

Metallurgy and Processing

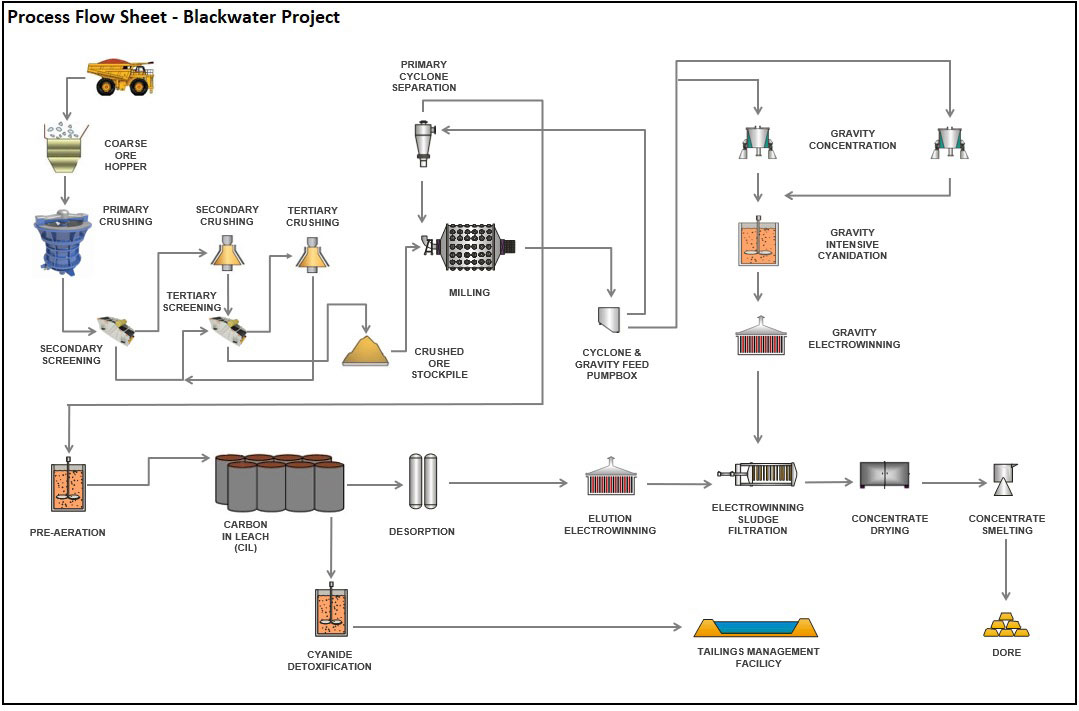

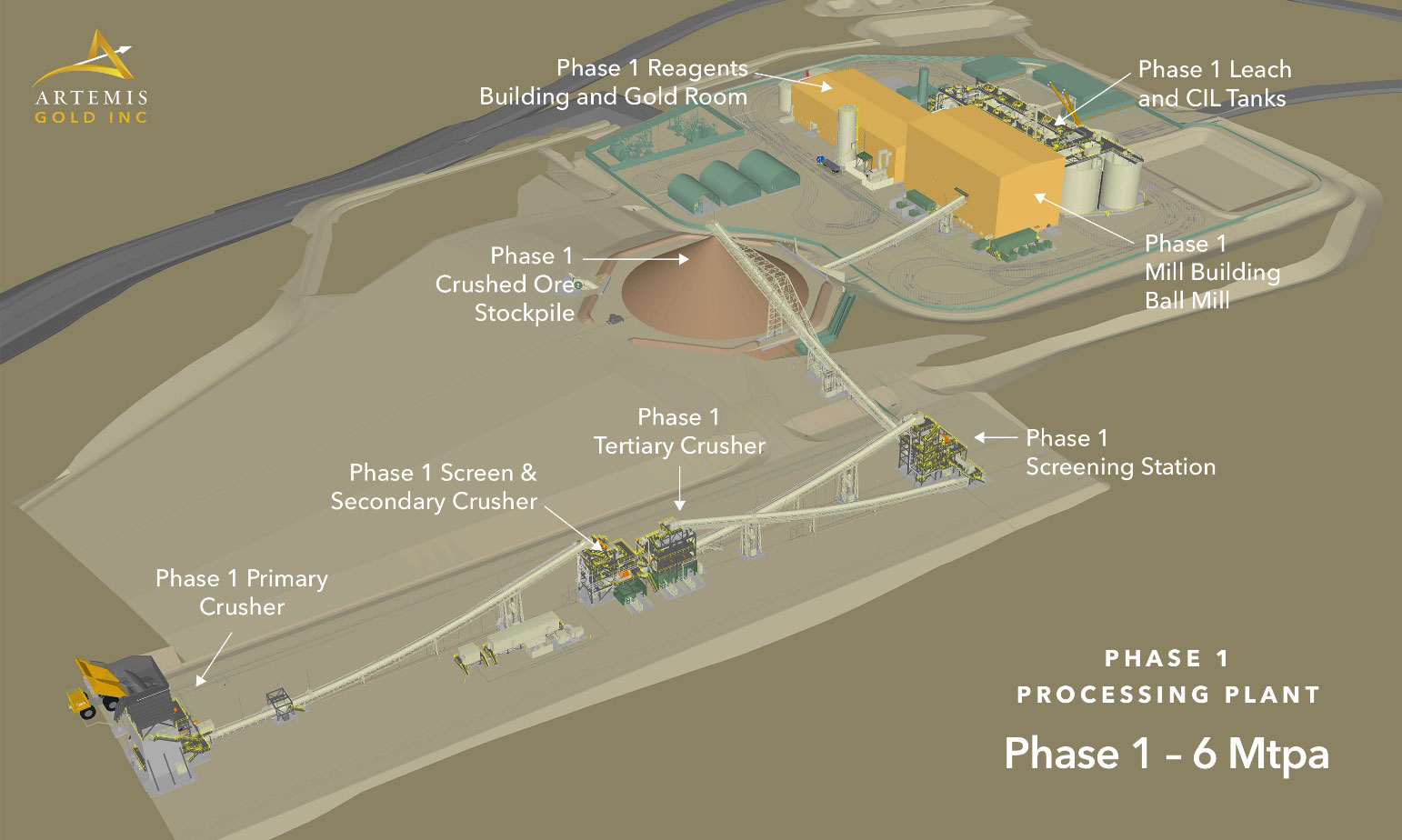

Phase 1

The processing plant for Phase 1 comprises the following:

- Three-stage crushing, consisting of a primary gyratory crusher, a secondary cone crusher and two tertiary cone crushers, each of which will be housed in stand-alone structures, with conveyors transporting material between each stage;

- Crushed product will be stored in a crushed ore stockpile and conveyed to a dual-drive variable-speed ball mill for grinding, with the circuit being closed by cyclones. Gravity concentration will be incorporated into the grinding circuit using two centrifugal concentrators. An intensive cyanide leach unit will be used for recovering gold from the gravity concentrate;

- The leach and adsorption circuits will consist of one pre-oxidation tank, two leach tanks and six CIL tanks fitted with mechanical agitators, with cyanide being added to the leach tanks and CIL tanks. The leach and adsorption circuit residence time will be 24 hours, with gravity flow between the pre-oxidation and leach tanks and interstage screens moving leached slurry between the tank units. The carbon will advance counter current to the main slurry flow during periodic transfers of slurry;

- The loaded carbon will be treated in an AARL elution and electrowinning circuit consisting of an acid wash column and an elution column operating at 120°C. An electric heating system will provide the necessary temperature, and two additional heat exchangers will control the temperature around the circuit. An electric-powered rotary kiln operating at approximately 750°C will be used to reactivate carbon. Electrowinning will be carried out to recover gold and silver from the elution solution and the resulting metallic values will be dried and smelted into doré bars;

- Cyanide destruction will be carried out in the final tailings slurry, using oxygen and the sulfur dioxide produced by the combustion of sulfur prill.

Figure 1 – Blackwater Phase 1 Process Flow Sheet

Figure 2 – Blackwater Phase 1 Design*

*This is an artist’s rendering illustrating Phase 1 of Blackwater Mine. This rendering may not be to scale, and the location of certain elements, materials and colours are subject to change.

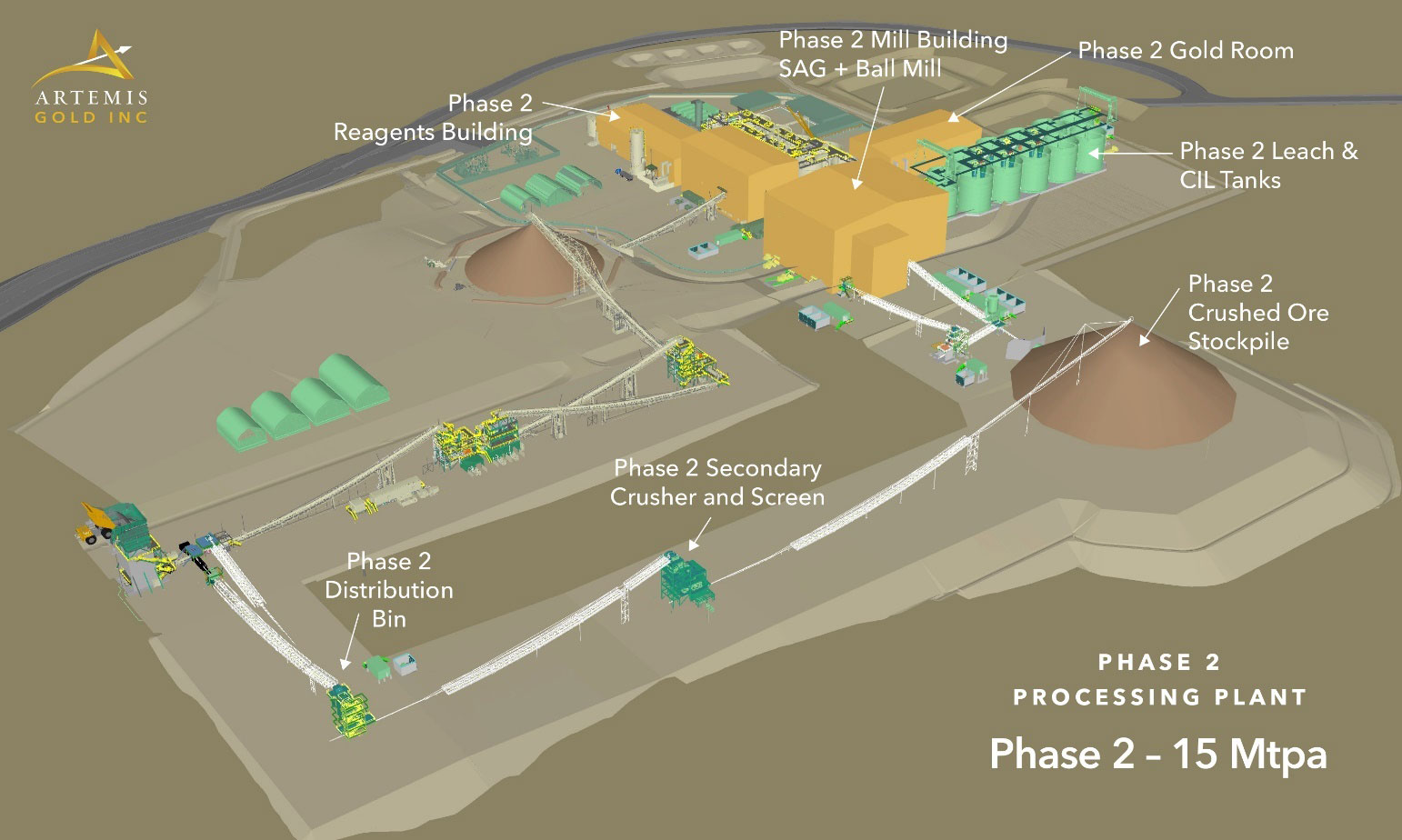

Phase 2 Expansion

The expansion study assumes the Phase 2 expansion to 15 Mtpa would be implemented with some modifications and upgrades to the Phase 1 process, including splitting the ore crushed in the primary crusher into two streams. One stream would be fed through the existing Phase 1 crushing and grinding circuits. Another stream would be processed with another secondary stage of crushing, stockpiling, followed by SAG and ball mill grinding. The rest of the plant circuits, including gravity concentration, leaching, adsorption, elution and cyanide destruction, as well as the process and reagent buildings would be expanded. Minor upgrades would be carried out on some infrastructure to accommodate the increased throughput. The capital cost estimate to complete the Phase 2 expansion is C$592 million.

Figure 3 – Blackwater Phase 2 Design*

*This is an artist’s rendering illustrating Phase 2 of Blackwater Mine. This rendering may not be to scale, and the location of certain elements, materials and colours are subject to change.

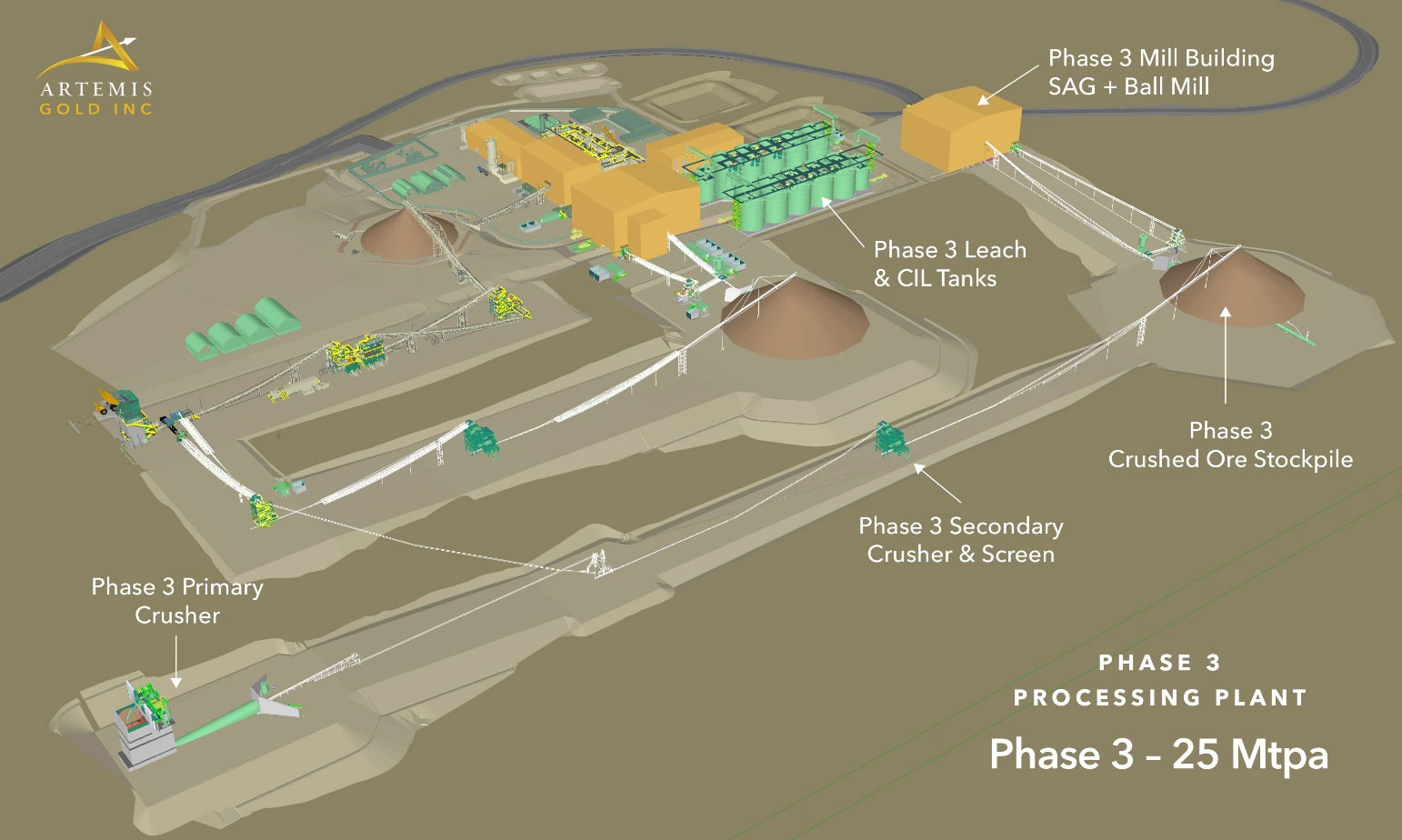

Phase 3 Expansion

The Phase 3 expansion to 25 Mtpa would require a new process line comprised of two-stage crushing, stockpiling, SAG and ball mill grinding and other plant circuits similar to the processing methods of Phases 1 and 2. The capital cost estimate to complete the Phase 3 expansion is C$852 million.

Figure 4 – Blackwater Phase 3 Design*

*This is an artist’s rendering illustrating Phase 3 of Blackwater Mine. This rendering may not be to scale, and the location of certain elements, materials and colours are subject to change.

A brief video illustrating the changes between Phases 1, 2, and 3 can be found here:

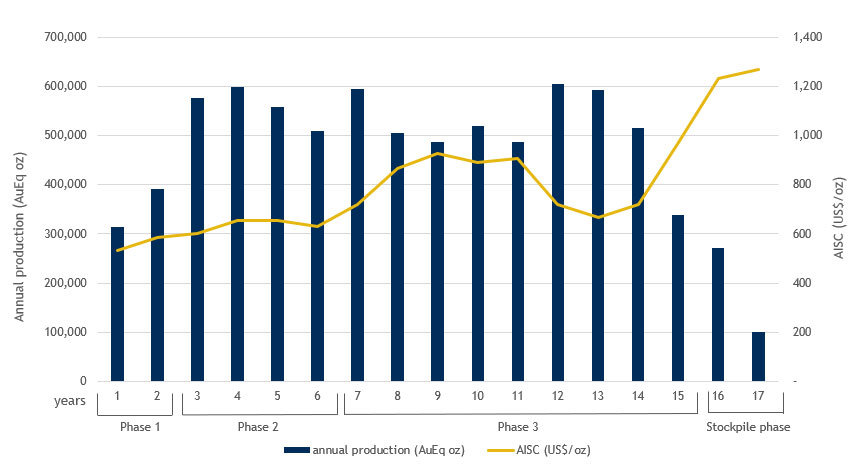

Production Profile and Costs

The average annual production per the expansion study is 469,000 AuEq oz at an average AISC of US$781 per gold oz, with average gold equivalent production of greater than 500,000 oz per annum throughout Phases 2 and 3. AuEq oz are determined using a gold:silver ratio of 78:1 (or US$1,800 to US$23).

Figure 5 – Blackwater Mine Gold Equivalent Production and AISC

Operating Costs

Phase 1 operating costs are estimated at C$28.67/t milled, with economies of scale driving down the processing and G&A costs to achieve an average estimated operating cost of C$20.03/t milled over the LOM.

Selling Costs

The expansion study assumes payable factors on gold and silver of 99.9% and 95%, respectively. Refining, treatment, transport, and insurance charges have been included at C$3/oz, applied to gold equivalent ounces.

Hedging and Commodity Price Assumptions

The expansion study reflects the impact of the Company’s hedge program in place as of the date of the study. This includes forward gold sales contracts to deliver a total of 190,000 ounces of gold bullion between March 2025 and December 2027 at a weighted average price of C$2,851/ounce, as well as zero cost collars for 30,000 oz gold with settlement dates from December 2024 to February 2025. The collars have a weighted average put price of C$2,600/oz and a weighted average call price of C$3,353/oz.

The commodity price assumptions for unhedged production and exchange rate assumptions in the expansion study were derived from market consensus forecasts and are as follows:

Table 3 – Commodity Price Assumptions

| Year 1 | Year 2 | Year 3 | Year 4 | Long-term | |

| Gold price (US$/oz) | US$2,000 | US$1,950 | US$1,900 | US$1,850 | US$1,800 |

| Silver price (US$/oz) | US$23 | US$23 | US$23 | US$23 | US$23 |

| Exchange rate (CAD:USD) | 0.74 | 0.74 | 0.74 | 0.74 | 0.74 |

Taxes

The expansion study includes estimates for the following taxes:

- British Columbia mining tax: 2% provincial minimum tax payable on net current proceeds which is creditable against the 13% effective mining tax rate which is calculated based on operating profit less applicable capital cost deductions. The mining tax is deductible in computing provincial and federal income tax;

- British Columbia provincial income tax: 12.0%, payable after applicable deductions are made;

- Canadian federal income tax: 15.0%, payable after applicable deductions are made.

Economic Outputs

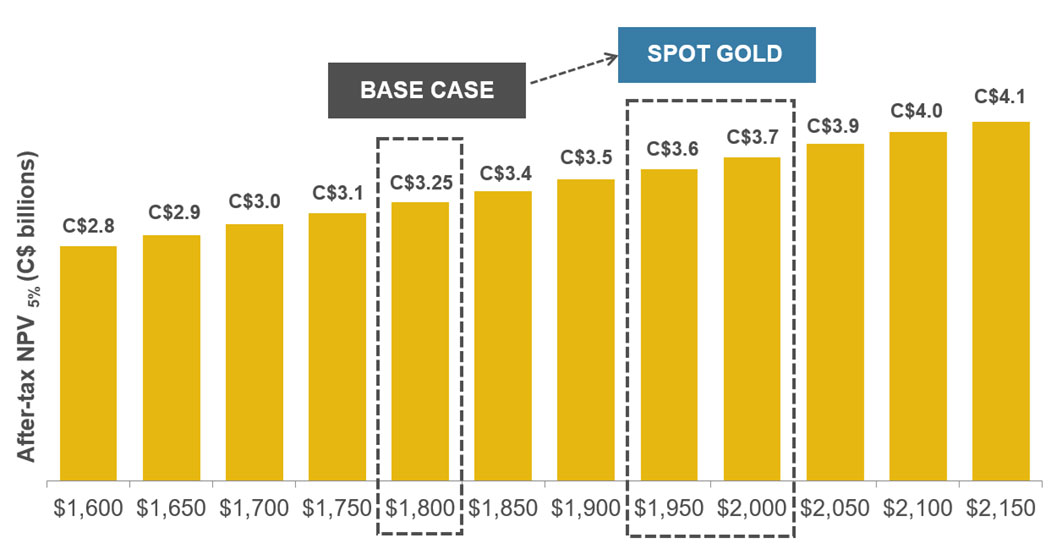

The expansion study returns a base case after-tax NPV5% of C$3.25 billion and takes into account the repayment of the PLF of $385 million, as well as the effect of the gold stream and silver stream arrangements.

Figure 6 – Sensitivity of Base Case After-tax NPV5% (C$ billions) to Changes in Long-term US$ Gold Price Holding the CAD:USD Exchange Rate Fixed at 0.74

Table 4 – Sensitivity on Base Case After-tax NPV5% (C$ Billions) to Changes in Long-term US$ Gold Price and CAD:USD Exchange Rate (base case highlighted)

| CAD:USD | Long-term gold price (US$/oz) | |||||||||||

| $1,600 | $1,650 | $1,700 | $1,750 | $1,800 | $1,850 | $1,900 | $1,950 | $2,000 | $2,050 | $2,100 | $2,150 | |

| 0.71 | $2.9 | $3.1 | $3.2 | $3.3 | $3.4 | $3.6 | $3.7 | $3.8 | $3.9 | $4.1 | $4.2 | $4.3 |

| 0.72 | $2.9 | $3.0 | $3.1 | $3.3 | $3.4 | $3.5 | $3.6 | $3.7 | $3.9 | $4.0 | $4.1 | $4.2 |

| 0.73 | $2.8 | $2.9 | $3.1 | $3.2 | $3.3 | $3.4 | $3.6 | $3.7 | $3.8 | $3.9 | $4.0 | $4.2 |

| 0.74 | $2.8 | $2.9 | $3.0 | $3.1 | $3.25 | $3.4 | $3.5 | $3.6 | $3.7 | $3.9 | $4.0 | $4.1 |

| 0.75 | $2.7 | $2.8 | $2.9 | $3.1 | $3.2 | $3.3 | $3.4 | $3.5 | $3.7 | $3.8 | $3.9 | $4.0 |

| 0.76 | $2.7 | $2.8 | $2.9 | $3.0 | $3.1 | $3.2 | $3.4 | $3.5 | $3.6 | $3.7 | $3.8 | $4.0 |

| 0.77 | $2.6 | $2.7 | $2.8 | $3.0 | $3.1 | $3.2 | $3.3 | $3.4 | $3.5 | $3.7 | $3.8 | $3.9 |

Artemis Gold Chairman and CEO Steven Dean commented: “The expansion study underlines that Blackwater is a true tier one asset, with gold equivalent production in excess of 500,000 ounces per year once Phase 2 is implemented, with lowest-decile operating costs, in a safe, stable and mining-friendly jurisdiction, as well as industry-leading ESG.”

The Study

The expansion study is led by Lycopodium Minerals Canada Ltd.(“Lycopodium”) together with Knight Piésold Ltd. (“KP”), Moose Mountain Technical Services (“MMTS”), ERM Consultants Ltd. (“ERM”), Lorax Environmental Services Ltd. (“Lorax”) and JAT MetConsult Ltd. (“JAT MetConsult”), all of which are independent of the Company.

An updated Technical Report will be filed on SEDAR+ within 45 days of this news release.

Data Verification

Data verification programs have included a review of QA/QC data, re-sampling and sample analysis programs, and database verification. Validation checks were performed on data, and comprise checks on surveys, collar coordinates and assay data.

In the opinion of MMTS, sufficient verification checks were undertaken on the database to provide confidence that the database is virtually error-free and appropriate to support Mineral Resource and Reserve estimation.

Additional Opportunities

The expansion study does not reflect the following additional opportunities which the Company continues to evaluate:

- Increased mine life – the current reserve estimate is based on a US$1,400/oz gold price. By applying a higher gold price for pit design and cut-off grade, some of Blackwater’s estimated resources could be converted into reserves and extend the mine life. The next steps would include re-running a pit optimization incorporating updated gold pricing and mine economics to assess the potential for increased reserves and mine life.

- Exploration of open resource extensions – past exploration data suggests Blackwater has additional exploration potential and that the resource is open to the North, Northwest and at depth. The Blackwater land package also remains largely under-explored. The next step will be to design an exploration program to test these extensions and the regional potential.

- Evaluation of alternative methods for transportation of waste material – the ex-pit haul route for waste material is expected to be relatively fixed for the LOM, opening up the possibility to perform hauling of waste material using alternative methods which may have the potential to significantly reduce operating costs and lower Blackwater’s greenhouse gas (“GHG”) emissions. The next steps will include further engineering and analysis, including engaging with the vendors of these systems.

- Electrification of the hauling fleet – the deployment of battery electric vehicles has the potential to significantly reduce operating costs and reduce Blackwater’s GHG emissions. The Company is currently working with Caterpillar Technology to assess the economic potential for incorporation of battery electric vehicles into the mine fleet.

- Automation of hauling operations – the potential to automate hauling operations presents an opportunity to optimize production efficiencies and reduce operating costs. The Company is currently undertaking the implementation of a fleet management system that would allow for potential automation of hauling operations in the future.

- Process engineering initiatives – as Blackwater starts producing more fresh rock ore at depth in the pit, the Company may evaluate alternative processing methodologies which may result in lower capital and operating costs for Phase 3. The next steps would include an assessment of alternatives, preliminary flowsheet design, and identification of any additional metallurgical test work required to support further engineering.

Conference Call and Webinar

Live

Artemis Gold will host a conference call and webinar on Thursday, February 22, 2024 at 9am PT (12pm ET). Participants may dial in using the numbers below (no access code is needed).

Toll-free (Canada and US): 1 844 763 8274

International: +1 647 484 8814

The webinar may be accessed here.

Archive

The conference call will be available for playback until end of day on March 22, 2024 by dialing the following numbers and entering access code 0719#.

Toll-free (Canada and US): 1 855 669 9658

International: +1 604 674 8052

The webinar will be archived on the Company’s website at www.artemisgoldinc.com.

Qualified Persons

The Qualified Persons that will prepare the Technical Report on the Study include: Sohail Samdani, P.Eng., (Lycopodium), Olav Mejia, P.Eng., (Lycopodium), Marc Schulte, P.Eng., (MMTS), Sue Bird, P.Eng. (MMTS), Daniel Fontaine, P.Eng. (KP), John A. Thomas, P. Eng. (JAT MetConsult Ltd.), Rolf Schmitt, P. Geo. (ERM) and John Dockrey, P. Geo. (Lorax). Each of the Qualified Persons has reviewed and approved the technical information contained in the expansion study and this news release in their area of expertise and is independent of the Company.

Jeremy Langford, FAUSIMM, a Qualified Person as defined by National Instrument 43-101, has reviewed and approved the Additional Opportunities section in this press release.

About Artemis Gold

Artemis Gold is a well-financed, growth-oriented gold development company with a strong financial capacity aimed at creating shareholder value through the identification, acquisition, and development of gold properties in mining-friendly jurisdictions. The Company’s current focus is the construction of the Blackwater Mine in central British Columbia, approximately 160km southwest of Prince George and 450km northeast of Vancouver. The project is one of the largest capital investments in the Bulkley-Nechako, Fraser-Fort George and Cariboo regions of B.C. in the last decade. The first pour of gold and silver from Blackwater Mine is expected in H2 2024. Artemis Gold trades on the TSX-V under the symbol ARTG. For more information visit www.artemisgoldinc.com.

On behalf of the Board of Directors

Steven Dean

Chairman and Chief Executive Officer

+1 604 558 1107

Investor Relations contact

Meg Brown

Vice President, Investor Relations

[email protected]

+1 778 899 0518

Media Relations contact

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Note Regarding Forward-looking Information

This press release contains certain forward-looking statements and forward-looking information as defined under applicable Canadian and U.S. securities laws. Statements contained in this press release that are not historical facts are forward-looking statements that involve known and unknown risks and uncertainties. Any statements that refer to expectations, projections or other characterizations of future events or circumstances contain forward-looking statements. In certain cases, forward-looking statements and information can be identified using forward-looking terminology such as “may”, “will”, “would”, “could”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans”, “potential” or similar terminology. Forward-looking statements and information are made as of the date of this press release, and include, but are not limited to, statements regarding the results of the expansion study, including but not limited to, anticipated average annual production and the costs thereof, average annual free cash flow and the re-optimization of contained resources and consequential mine life extension; the potential of the Blackwater Mine; long term gold prices; the optimization of mine expansion and the funding thereof; expectations with respect to a development decision at the Blackwater Mine; the infrastructure requirements at the Blackwater Mine and the costs thereof; anticipated mining methods at the Blackwater Mine and the duration thereof; metallurgy and processing at the Blackwater Mine; the jobs to be created in connection with the project; alternative methods for transportation of waste material; the electrification of the hauling fleet; the potential to automate hauling operations; the potential evaluation of alternative processing methodologies; agreements and relationships with Indigenous partners; the future of mining in British Columbia; the plans of the Company concerning the project, including construction, site preparation, clearing, consultation with indigenous groups, and other plans and expectations of the Company concerning the project.

These forward-looking statements represent management’s current beliefs, expectations, estimates and projections regarding future events and operating performance, which are based on information currently available to management, management’s historical experience, perception of trends and current business conditions, expected future developments and other factors which management considers appropriate. Such forward-looking statements involve numerous risks and uncertainties, and actual results may vary. Important risks and other factors that may cause actual results to vary include, without limitation: risks related to the ability of the Company to accomplish its plans and objectives with respect to the development of the project within the expected timing or at all, the timing and receipt of certain required approvals, changes in commodity prices, changes in interest and currency exchange rates, risks inherent in exploration estimates and results, risks inherent in exploration and development activities, changes in development or mining plans due to changes in logistical, technical or other factors, unanticipated operational difficulties (including failure of plant, equipment or processes to operate in accordance with specifications, cost escalation, unavailability of materials, equipment or third party contractors, delays in the receipt of government approvals, industrial disturbances, job action, and unanticipated events related to heath, safety and environmental matters), changes in governmental regulation of mining operations, political risk, social unrest, changes in general economic conditions or conditions in the financial markets, and other risks related to the ability of the Company to proceed with its plans for the project and other risks set out in the Company’s most recent MD&A, which is available on the Company’s website at www.artemisgoldinc.com and on SEDAR+ at www.sedarplus.ca.

In making the forward-looking statements in this press release, the Company has applied several material assumptions, including without limitation, the assumptions that: (1) market fundamentals will result in sustained mineral demand and prices; (2) any necessary approvals and consents in connection with the development of the project will be obtained; (3) financing for the development, construction and continued operation of the project will continue to be available on terms suitable to the Company; (4) sustained commodity prices will continue to make the project economically viable; (5) there will not be any unfavourable changes to the economic, political, permitting and legal climate in which the Company operates; (6) anticipated metallurgical recoveries will be achieved; (7) refining and offtaking arrangements will be concluded on terms equivalent to those assumed in the expansion study; (8) forecasted operating and capital cost will not be materially different from the assumptions in the expansion study; and (9) that the tax benefits assumed in the expansion study will be realized. Although the Company has attempted to identify important factors that could affect the Company and may cause actual actions, events, or results to differ materially from those described in forward-looking statements, there may be other factors that cause the actual results or performance by the Company to differ materially from those expressed in or implied by any forward-looking statements. Accordingly, no assurances can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what impact they will have on the results of operations or the financial condition of the Company. Investors should therefore not place undue reliance on forward-looking statements. The Company is under no obligation and expressly disclaims any obligation, to update, alter or otherwise revise any forward-looking statement, whether written or oral, that may be made from time to time, whether because of new information, future events or otherwise, except as may be required under applicable securities laws.

Non-IFRS Performance Measures

The Company has included certain non-IFRS measures in this news release. The company believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the project. The non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures do not have any standardized meaning prescribed under IFRS and therefore may not be comparable with other issuers.

Cash Costs

Cash costs are a common financial performance measure in the gold mining industry but with no standard meaning under IFRS. Artemis Gold considers and discloses cash costs on a sales basis. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, such as sales, certain investors use this information to evaluate the project’s performance and ability to generate operating earnings and cash flow from its mining operations. Management uses this metric as an important tool to monitor cost performance.

Cash costs in the Study include production costs such as mining, processing, refining and site administration, less revenue generated from silver sales and adjustments to stockpile inventory, divided by gold ounces sold to arrive at cash costs per gold ounce sold. Costs include royalty payments, permitting costs, and payments that are expected to be made to Indigenous Nations. Other companies may calculate this measure differently.

All-in Sustaining Costs

The Company believes AISC more fully defines the total costs associated with producing gold. The Company calculated AISC for the Study as the sum of cash costs (as described above), sustaining capital and closure costs, all divided by the gold ounces sold to arrive at a per-ounce figure. Other companies may calculate this measure differently because of differences in underlying principles and policies applied. Differences may also arise due to a different definition of sustaining versus growth capital.

Note that in respect of AISC metrics within the Study, as such economics are disclosed at the project level, corporate general and administrative expenses were not included in the AISC calculations.

Appendix

Table A – Average Proposed Annual Mine Production for the Blackwater Mine – Expansion Study

Table B – Operating and Financial Results of Expansion Study by Phase

| Phase 1 | Phase 2 | Phase 3 | Stockpile Phase9 | LOM | |

|---|---|---|---|---|---|

| Years | 1-2 | 3-6 | 7-15 | 16-17 | 17 |

| Growth capital1, 2 | $53m | $592m | $852m | n/a | $1,497m |

| Sustaining capital2 | $140m | $457m | $498m | $28m | $1,122m |

| Throughput capacity (Mtpa) | 6.0 | 15.0 | 25.0 | 25.0 | Variable |

| Gold grade (g/t) | 1.51 | 1.18 | 0.65 | 0.30 | 0.75 |

| Silver grade (g/t) | 7.59 | 7.87 | 4.96 | 6.75 | 5.78 |

| Gold equivalent grade (g/t)3 | 1.57 | 1.25 | 0.69 | 0.36 | 0.79 |

| Gold recoveries | 93% | 93% | 93% | 93% | 93% |

| Average annual gold production (oz) | 338,000 | 530,000 | 483,000 | 155,000 | 438,000 |

| Average annual silver production (oz) | 1,190,000 | 2,468,000 | 2,590,000 | 2,418,000 | 2,376,000 |

| Average annual AuEq production (oz)4 | 353,000 | 561,000 | 516,000 | 186,000 | 469,000 |

| Strip ratio (waste:ore) | 1.89 | 2.00 | 2.03 | n/a | 2.01 |

| Operating costs ($/tonne milled) | $28.67 | $25.80 | $19.02 | $12.83 | $20.03 |

| Cash costs5 (US$/oz) | US$408 | US$477 | US$722 | US$1,173 | US$645 |

| AISC6 (US$/oz) | US$561 | US$637 | US$807 | US$1,240 | US$781 |

| Average annual free cash flow7 | $536M | $544M | $414M | $109M | $413M |

| After-tax NPV5%8 | $3.25B |

Notes

- Includes deferred initial capex

- Excludes closure costs and salvage value

- Gold equivalent grades have been determined using a gold price of US$1,800/oz, a silver price of US$23/oz, a gold metallurgical recovery of 93%, a silver metallurgical recovery of 65%, and mining smelter terms for the following equation: AuEq = Au g/t + (Ag g/t x 0.0085)

- Gold equivalent ounces have been determined using a gold-to-silver ratio of 78:1 (US$1,800:US$23)

- Cash costs include selling costs, royalty payments, operating costs, less silver by-product credits and adjustments to stockpile inventory, divided by payable gold ounces

- AISC includes cash costs as defined above, sustaining capital and closure costs, divided by payable gold ounces

- Free cash flow = operating cash flow less sustaining capex, closure costs and taxes

- After-tax NPV represent the net present value of after-tax project cash flows, discounted at a rate of 5%. The after-tax project cash flows take into account the repayment of the PLF of $385 million, as well as the effect of the gold stream and silver stream arrangements.

- Stockpile Phase involves the processing of low-grade ore stockpiles mined during Phases 1-3

Table C – Operating Costs by Phase

| units | Phase 1 | Phase 2 | Phase 3 | Stockpile Phase | LOM | |

| Mining* | $/t mined | 2.46 | 2.15 | 2.78 | n/a | 2.57 |

| Processing | $/t milled | 10.51 | 10.06 | 9.80 | 9.83 | 9.88 |

| G&A | $/t milled | 5.30 | 3.43 | 2.41 | 1.90 | 2.67 |

* Mining costs excludes the cost of major component replacements which are reported as sustaining capital and include low-grade ore stockpile rehandle. LOM mining costs exclude taxespre-stripping.